Supervised Learning Performance Measurement: Regression Models

Search for a command to run...

No comments yet. Be the first to comment.

Deploying a .NET application to a cloud environment like DigitalOcean is a powerful way to ensure scalability, reliability, and ease of management. In this post, we’ll walk through deploying a real-world .NET application—a simple ASP.NET Core MVC app...

Building a gRPC Service in C# and ASP.NET Core – Part 2

Building a gRPC Service in C# and ASP.NET Core – Part 1

Software architecture is the backbone of any application, and a well-thought-out architecture can make the difference between a maintainable, scalable application and a fragile, difficult-to-modify one. Clean Architecture, popularized by Robert C. Ma...

In software development, as systems grow more complex, objects start interacting with each other in increasingly intricate ways. Over time, this can lead to a tightly coupled, hard-to-maintain system where modifying or extending a particular feature ...

Let's quickly review the two categories of supervised learning models: regression models and classification models. Regression models predict a continuous dependent variable, such as an integer result. On the other hand, classification models predict a class result, like whether a student will pass an exam or not. For this article, we will focus on regression models.

Once we have created our model, it is important to assess its performance in a real-world setting. This involves checking for overfitting or underfitting and determining the level of accuracy we can expect. Performance measurements are used to evaluate our models and their reliability. There are several metrics available to measure regression model performance, such as MSE, RMSE, MAE, R-squared, and Adjusted R-squared. In this article, we will focus on these commonly used metrics.

The mean square error gives us an average of the variance of our model.

It is calculated using the formula:

Ỹ - the predicted value of our model

Y - the actual value of our model

n - the number of data points (row)

Implementation in Python

def mean_squared_error(predictions, targets):

if len(predictions) != len(targets):

raise ValueError("Input lists must have the same length")

squared_errors = [(p - t) ** 2 for p, t in zip(predictions, targets)]

mse = sum(squared_errors) / len(predictions)

return mse

predicted_values = [2.5, 3.7, 4.8, 6.1, 7.3]

actual_values = [2.1, 3.8, 5.0, 5.9, 7.2]

mse = mean_squared_error(predicted_values, actual_values)

print("Mean Squared Error:", mse)

Our RMSE Metric builds on the aforementioned MSE metric. With the addition of taking the square root of the MSE (to return the value to the original unit before it was squared in MSE)

It is calculated with this formula:

Implementation in Python

import math

def root_mean_squared_error(predictions, targets):

if len(predictions) != len(targets):

raise ValueError("Input lists must have the same length")

squared_errors = [(p - t) ** 2 for p, t in zip(predictions, targets)]

mean_squared_error = sum(squared_errors) / len(predictions)

rmse = math.sqrt(mean_squared_error)

return rmse

predicted_values = [2.5, 3.7, 4.8, 6.1, 7.3]

actual_values = [2.1, 3.8, 5.0, 5.9, 7.2]

rmse = root_mean_squared_error(predicted_values, actual_values)

print("Root Mean Squared Error:", rmse)

Similar to the MSE metric, instead of calculating the square of the difference between the actual and predicted, we take the absolute difference.

Implementation in Python

def mean_absolute_error(predictions, targets):

if len(predictions) != len(targets):

raise ValueError("Input lists must have the same length")

absolute_errors = [abs(p - t) for p, t in zip(predictions, targets)]

mae = sum(absolute_errors) / len(predictions)

return mae

predicted_values = [2.5, 3.7, 4.8, 6.1, 7.3]

actual_values = [2.1, 3.8, 5.0, 5.9, 7.2]

mae = mean_absolute_error(predicted_values, actual_values)

print("Mean Absolute Error:", mae)

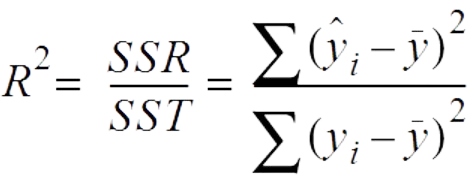

R-squared (Coefficient of Determination) is a statistical measure that represents the proportion of the variance for the dependent variable (target) that's explained by independent variables (predictors) in a regression model. It provides an indication of the goodness of fit of a regression model to the observed data points. In other words, R-squared tells you how well the regression line fits the data points.

The R-squared value ranges from 0 to 1. Here's what it indicates:

R-squared = 0: The model explains none of the variance in the dependent variable. It doesn't fit the data at all.

R-squared = 1: The model explains 100% of the variance in the dependent variable. It perfectly fits the data.

Implementation in Python

from sklearn.linear_model import LinearRegression

from sklearn.metrics import r2_score

# Example data

X = [[1], [2], [3], [4], [5]]

y = [2, 3.9, 6.1, 8.0, 9.8]

# Create and fit a linear regression model

model = LinearRegression()

model.fit(X, y)

# Predict the target values

y_pred = model.predict(X)

# Calculate R-squared

r_squared = r2_score(y, y_pred)

print("R-squared:", r_squared)

Adjusted R-squared is a modified version of the regular R-squared (Coefficient of Determination) that takes into account the number of predictor variables in a regression model. While R-squared measures the proportion of the variance in the dependent variable explained by the independent variables, Adjusted R-squared adjusts this value based on the number of predictors and the sample size.

The idea behind Adjusted R-squared is to penalize the inclusion of unnecessary variables that might artificially inflate the R-squared value. As more predictor variables are added to a model, the R-squared value tends to increase even if those variables don't contribute significantly to the model's predictive power. Adjusted R-squared provides a more balanced assessment of a model's goodness of fit, especially when comparing models with different numbers of predictors.

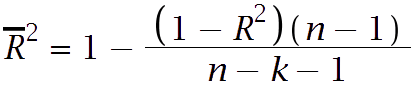

Mathematically, the Adjusted R-squared is calculated using the following formula:

Where:

( R^2 ) is the regular R-squared value.

( n ) is the number of observations (sample size).

( k ) is the number of predictor variables in the model.

Adjusted R-squared will always be lower than or equal to the regular R-squared. If the model adds meaningful explanatory power, the Adjusted R-squared will increase; if it adds little or no explanatory power (or if it overfits), the Adjusted R-squared will decrease or stay the same.

Implementation in Python

import numpy as np

import statsmodels.api as sm

# Example data

X = np.array([[1, 2], [2, 3], [3, 4], [4, 5], [5, 6]])

y = np.array([3, 6, 8, 10, 12])

# Add a constant term to the predictor matrix

X = sm.add_constant(X)

# Create and fit a linear regression model

model = sm.OLS(y, X).fit()

# Calculate Adjusted R-squared

adjusted_r_squared = 1 - (1 - model.rsquared) * (len(y) - 1) / (len(y) - X.shape[1] - 1)

print("Adjusted R-squared:", adjusted_r_squared)

It is important to measure performance in order to determine the quality of our model and identify areas for improvement. The metrics mentioned above are particularly relevant when working with linear regression models.